We’re often asked what is the best way to choose a pet insurance company. Well, there are a couple of ways to go. You can either start by asking yourself some questions. What type of coverage do you need? Do you want a plan that covers accidents only, or do you want a plan that covers accidents and illnesses? Do you want a plan that includes wellness care? You can also do some research to see what each insurance provider offers. If we’re honest, this route will take you a lot of time and energy.

The much easier way to choose a pet insurance plan is to use our website. We rank the best pet insurance companies by sifting through over 150,000 honest reviews from pet parents just like you. According to our most recent findings, the following are the best pet insurance companies of April 2024:

Our Process

When it comes to recognizing best pet insurance companies in the industry, we’ve got a bit of an advantage. Every month, pet parents just like you use our website to not only search for providers, but to also leave honest reviews of the companies they’ve chosen.

And each month we track this data to rank the top 10 pet insurance providers. We add together each insurer’s overall ratings scores and divide that score by the total number of reviews we have received for that insurer to give an overall average score. We are thrilled to find that so many pet insurance companies seem to be getting a lot of things right! And according to our customers, the following 10 providers are the absolute best pet insurance companies for April 2024.

Trupanion

Coming in at #1 is Trupanion. With over 50,000 reviews and an overall score of 4.9 out of 5 by our customers, it’s easy to see why they have been ranked as one of the best pet insurance companies of 2023.

Trupanion offers pet insurance policies for cats and dogs that cover accidents and illnesses. Currently, there is no coverage for exotic pets such as birds, reptiles or small mammals.

This provider’s standard plans will cover breed-specific and congenital issues. Pet parents can also opt for add-on policies that cover things like damage done by your pet to someone else’s property, boarding fees should you be hospitalized, rehabilitation and alternative therapies like acupuncture.

Trupanion offers a wide range of premium and deductible options. For instance, their deductibles range from $0 to $1,000. Keep in mind that pet insurance works like human health insurance. The lower your deductible, the higher your monthly premiums will be.

Something that really sets Trupanion apart from other providers on this list is that they don’t have any coverage limits. Often a pet insurance company will have either annual or per condition payout limits, but not Trupanion. They do not, however, cover pre-existing conditions.

Here is a recent review we received from a customer about Trupanion:

Pros:

- Covers breed-specific conditions and congenital conditions

- Short waiting period of 5-days for injuries

- No payout limits

- Wide range of deductible/premium options

Cons:

- Longer waiting period for illnesses coverage

- No coverage for exotic pets

- Exam fees and preventive care are not covered

The Final Verdict:

Trupanion offers accident and illness coverage for dogs and cats. Pet parents also have the option of adding coverage for rehab and alternative therapies. Their policies have no coverage limits and offer a broad range of deductible options to choose from.

You can find out more information from their website.

Lemonade

Lemonade takes the #2 spot receiving a score of 4.9 out of 5 from our customers. One of the things that sets this provider apart is the fact they use a non-traditional insurance model. To start, they rely on Artificial Intelligence and what is called “behavioral economics” to replace traditional brokers and bureaucracy. They also take a flat fee from monthly premiums, use the rest to pay the claims, and donate the remaining funds to a charity selected by their customers.

This new insurance model means Lemonade is able to provide customers with great service and very low monthly premiums. In fact, Lemonade’s sample $11 monthly cat insurance premium and $19.44 sample monthly dog insurance premium are some of the lowest of all the providers on our list. Additional savings can be earned by covering multiple pets, making annual payments, or bundling more than one insurance product.

Lemonade’s policies cover vet costs resulting from illness or accidents and include things like diagnostic testing, emergency care, surgery, hospitalization and medications. Pet parents are also able to choose from three preventative care packages to cover expenses from wellness exams, dental cleanings, routine blood tests and spaying and neutering.

Like most other pet insurance providers, Lemonade does not cover any pre-existing conditions.

Here’s just one of the recent Lemonade reviews left by one of our users:

Pros:

- Low monthly premiums

- Offers three different preventative care packages

- Multiple discounts are available

- Great customer service

Cons:

- Available in only 35 states and the District of Columbia

- No coverage for exotic pets

The Final Verdict:

Lemonade sells incredibly affordable pet insurance for dog and cat parents. They also pride themselves on awesome customer service and cutting out unnecessary bureaucracy. Oh, and they donate to charity! While they are currently only providing coverage in 35 states, they are continuing to expand.

You can find out more information from their website.

Healthy Paws

Coming in hot at number three is Healthy Paws pet insurance. With over 7,000 verified reviews and an overall score of 4.9 out of 5, Healthy Paws was rated the best pet insurance company by customers in 2015, 2016 and 2017 at Petinsurancereview.com, Consumersadvocate.org, PetInsuranceQuotes.com and other leading review sites.

Healthy Paws likes to keep things as simple as possible. That’s why they offer one simple plan that covers cat and dog accidents and illness with no per incident, annual or lifetime payout limits. They are another insurance provider that believes in giving back. With each pet insurance quote submitted, Health Paws makes a donation to a pet rescue or animal shelter through its Every Quote Gives Hope™ medical grant program.

Most claims are processed within 10 days and Healthy Paws has taken the paper work and traditional claims form out of the picture. Customers can simply snap a photo of the vet bill and submit the image through the Healthy Paws app or through their website.

Here is a recent review for Healthy Paws from one of our customers:

Pros:

- No coverage limits

- Pet parents can use any licensed veterinarian in the country

- Vet bills may be submitted through their mobile app or website

Cons:

- No coverage for exotic pets

- Pets enrolled before the age of 6 will experience a 12-month waiting period for hip dysplasia

- A $25 admin fee to initially set up your account

The Final Verdict:

Healthy Paws offers accident and illness coverage for cats and dogs. No need for typical claims forms to be filled out. Simply upload an image of your bill and be paid within 10 days.

You can find out more information from the Healthy Paws website.

Prudent Pet

At number 4, Prudent Pet is a newer kid on the block but has already received an overall score of 4.8 out of 5 from our customers. Founded in 2018, the company offers two plans, plus a comprehensive package that involves unlimited yearly coverage for vet costs, as well as reimbursements for some covered items that many other providers don’t. For instance, lost pet ads and holiday cancellation fees.

Prudent Pet offers accident-only coverage for as little as $10 per month and accident and illness coverage for as little as $16. These are some of the absolute lowest monthly premiums around. It should be noted with Prudent Pet and all providers on this list, coverage costs are based on your pet’s age, breed, and zip code.

Here is what one of our customers had to say about Prudent Pet:

Pros:

- An option for unlimited annual benefits

- Additional coverage may be added on

- No age or breed restrictions

- 24/7 vet support

Cons:

- Longer wait times for reimbursement – up to 30 days

- Annual health exams required

- Annual benefit limits not customizable

The Final Verdict:

A newer provider, Prudent Pet is already making waves in the industry by offering top coverage along with some pretty sweet extras not offered by many others. Monthly premiums are some of the lowest we’ve seen, and certain plans offer unlimited annual benefits.

Find out more from the Prudent Pet website.

Fetch by The Dodo

In our 5th spot is Fetch by The Dodo with an overall score of 4.7 out of 5 from our customers. Fetch stands out as the pet insurance recommended by the #1 animal brand in the world.

Fetch offers a comprehensive accident and illness plan, however they do not offer a wellness plan to cover things like vaccinations and teeth cleaning. Having said that, they do offer coverage that many other providers don’t for things like behavioral issues, alternative and holistic therapies, and boarding fees if you are hospitalized. Fetch even covers virtual vet visits up to $1,000 each year without a copay.

Another nice thing about fetch is that they offer multiple ways for pet parents to save on their premiums. You have the option of avoiding installment fees by choosing to pay quarterly or annually. There is no multi-pet discount, but Fetch does offer discounts for pets adopted from a rescue shelter, as well as to active duty and veterans and AARP members.

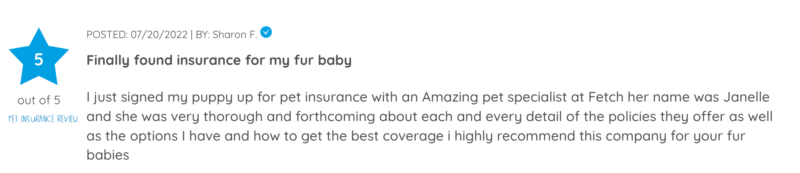

Here is a recent review for Fetch left by one of our customers:

Pros:

- Exam fees are covered

- Earn up to 30% off premiums with Healthy Pet Credit

- Coverage included for behavior, alternative therapies, boarding fees, and vet-recommended supplements

Cons:

- No wellness plan option

- No exotic pets covered

- Coverage renewal requires annual wellness visit

The Final Verdict:

Fetch by The Dodo offers pet parents a comprehensive accident and illness plan. While it doesn’t offer a wellness plan, you are able to cover some things other providers won’t cover. Fetch also has multiple ways to save on monthly premiums.

Get more information from their website.

Spot

Ranked number 6 by our customers, Spot has a 4.8 out of 5 rating. Spot offers an accident-only plan, or an accident and illness plan for cats and dogs. Policies come with annual deductibles and annual coverage limits.

Spot stands out from other providers because their basic insurance plan not only covers major procedures like surgeries and prescription medications, but also diagnostic exams and alternative treatments like chiropractic and hydrotherapy. Their basic plan does not cover wellness care, but Spot does offer two preventative care packages (Gold Preventative and Platinum Preventative) to cover all of your bases.

Spot also offers a multi-pet discount.

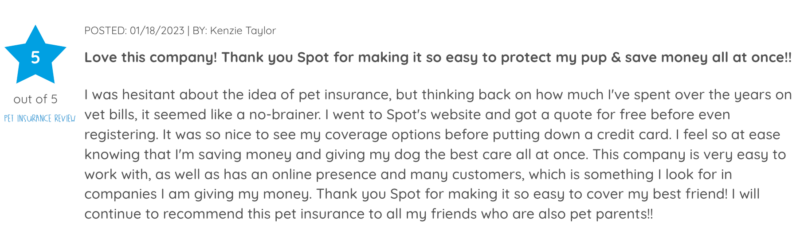

Here is a recent review by one of our customers:

Pros:

- Choice of accident and illness policies or accident-only plans

- Unlimited coverage option

- Exam fees related to accident/illness reimbursed

- Multi-pet discount

Cons:

- No wellness exams covered (but option to buy add-on packages)

- No exotic pets

The Final Verdict:

Spot pet insurance offers accident-only coverage or accident and illness coverage. Pet parents can also buy additional packages to cover preventative care. And Spot will help you save money if you enroll more than one pet.

Find out more about Spot by visiting their website.

Embrace

Number 7 on our list of top 10 pet insurance companies of January 2023 is Embrace. Embrace offers a comprehensive accident and illness plan as well as an additional Wellness Rewards program. Their Wellness plan is non-insurance based but it will help you cover the cost of routine exams, teeth cleaning, spaying and neutering and more.

Embrace offers a multi-pet discount of 10%. Plus, for each year a pet parent does not submit a claim, Embrace will decrease your deductible by $50. Claims can be submitted through Embrace’s app, as well as by email, fax or regular mail.

Something that really sets Embrace apart is that they have one of the shortest waiting times of all of the companies on our list. They have a two-day waiting period for accidents. Their 14-day waiting period for illnesses is pretty standard.

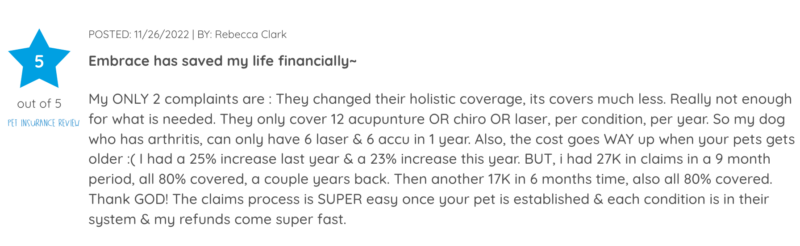

Here is what one of our customers had to say about their experience with Embrace:

Pros:

- Claims submitted easily through mobile app

- Short two-day waiting period for accidents

- Decreasing deductibles for zero claim reimbursements

Cons:

- No coverage for exotic pets

- No wellness or preventative care coverage

The Final Verdict:

Embrace offers insurance plans for dogs and cats. While no wellness coverage is included, pet parents are able to buy their Wellness Rewards plan that will cover the costs of check-ups, spaying/neutering, and even grooming and training.

For more information, visit Embrace’s website.

Hartville

At number 8, Hartville has been given an overall score of 4.7 out of 5 by our users. This provider offers coverage for dogs and cats ages eight weeks and up in all 50 states, as well as the District of Columbia. They also offer two main policies: an accident-only policy and an accident and illness policy.

Their accident and illness plan is comprehensive and covers costs associated with accidents and illness, even hereditary issues. The great thing about this plan is that it also covers costs associated with behavioral issues, alternative treatments like acupuncture, and even chemotherapy. Often pet parents need to purchase an additional plan for these expenses.

For those who are on a tight budget and looking for a way to save, the accident-only plan is the way to go. This plan covers things like broken bones, ingesting something toxic or obstructive and more. And the best part is, should your finances change, you can always add more comprehensive services at any time.

And for those pet parents looking to cover the typical costs of routine check-ups and wellness care, Hartville also has two optional preventative-care packages.

Here is a user review about Hartville:

Pros:

- Affordable plans

- Comprehensive coverage

- Unrestricted vet selection

- Out of state coverage

- Multi-pet discount

Cons:

- No exotic Pets

- Coverage doesn’t start until the 15th day after the policy’s effective date.

The Final Verdict:

Hartville is offered to pet parents in all 50 states. Their comprehensive accident and illness policy is one of the best on this list and covers costs for things like behavioral issues, alternative treatments, and even chemotherapy. They also offer a more affordable accident-only policy, as well as preventative packages.

You can find out more about Hartville from their website.

Pet Partners

Coming in in 9th place with an overall rating of 4.7 out of 5 stars is Pet Partners. Founded in 2002, Pet Partners was one of the first pet insurance companies in the country and they have been offering customizable plans in all 50 states since that time. Customizable plans allow pet parents to choose the right premiums, deductibles and reimbursement options.

There are a couple of things that make this provider stand out. To start, while they have been in business in the US since 2002, the company was involved in pet insurance in the UK since the 1980s. You could say they have learned exactly what pet parents want and need in coverage.

Another thing that sets Pet Partners apart is that they are the official insurance provider for both the American Kennel Club (AKC) and the Cat Fanciers’ Association. It’s not surprising this provider has made our list of best pet insurance companies of 2022!

An accident and illness plan can cost pet parents as little as $10 a month. Keep in mind, as with other pet insurance providers, premiums are based on a variety of factors, including the pet’s age, breed, and zip code.

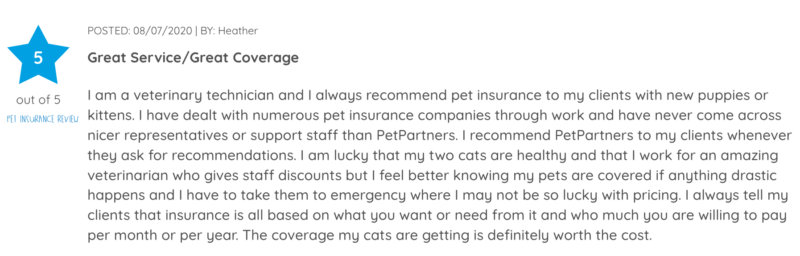

Here is what one of our users had to say about Pet Partners:

Pros:

- Customizable policies

- Low base premiums (some of the lowest in this group)

- Multi-pet discount

- Extensive experience in the pet insurance industry

Cons:

- No wellness plans

- Limited options for older pets (PetPartners removes some coverage options for new enrollments starting at age five and limits plans entirely for pets aged nine and up.)

The Final Verdict:

Pet Partners has been around a long time, and the fact they are the official insurer of the AKC and the Cat Fancier’s Association says a lot. Rates are low and plans are customizable, which means you can find something that will fit your specific budget.

Find out more about Pet Partners.

ASPCA

And to round out our top 10 best pet insurance companies of January 2023 is ASPCA, with an overall rating of 4.7 out of 5 from our users. Their Complete Coverage plan covers accidents, injuries and illnesses, and features a simplified reimbursement based on percentage of invoice. Pet parents also have the option of adding on additional preventative care coverage.

Not only do their plans cover the typical issues like surgery, hospitalizations and emergency vet care, they also cover cancer treatments, holistic/alternative care, and behavioral therapy. And they are one of the few that will even cover the costs of stem cell treatment. They also offer additional coverage for preventative care.

ASPCA is also great when it comes to pre-existing conditions. Once a pet heals and no longer displays symptoms for 180 days, coverage may be offered. They also have no upper age limit for enrollment.

ASPCA’s Complete Coverage and Accident Only policies have annual deductibles and annual coverage limits. Those limits will reset at the beginning of the new policy year.

If you are the parent of horses, along with cats and dogs, you’ll be happy to hear ASPCA sells insurance for horses as well. That’s unique to the companies on this list.

A bit of a negative is that claims processing time is on the high end with this provider, up to 30 days.

Here is what one of our users had to say about ASPCA:

Pros:

- Provides illness/injury coverage (including holistic/alternative therapies)

- Horses can also be covered

- Offers options for preventative care

Cons:

- Claims may take up to 30 days

The Final Verdict:

ASPCA Pet Health Insurance offers comprehensive coverage for illnesses and injuries, including holistic/alternative therapies. They also offer policies for horses.

For more information, visit their website.

Final Thoughts

We would like to take this opportunity to thank all of our users who have left thoughtful reviews on our website. By taking the time to provide this feedback, we are able to consistently rank the best pet insurance companies and help other pet parents choose the very best policies for them and their fur babies. This means pets are able to get the care they need when they need it, and pet parents have the financial support they need in a crisis.

As an added bonus, these reviews also help us generate revenues from the insurers, allowing us to donate a portion of earnings to charity!